The new W-4 form has proved itself to be quite the obstacle for small business owners. Rather than debate the functionality, ease of use, or practical application of it, we just want to dive right in and tell you how to use it. While the post is written for small business owners, employees themselves will benefit from this article. So here are the vital things you need to know about the new W-4.

A little background:

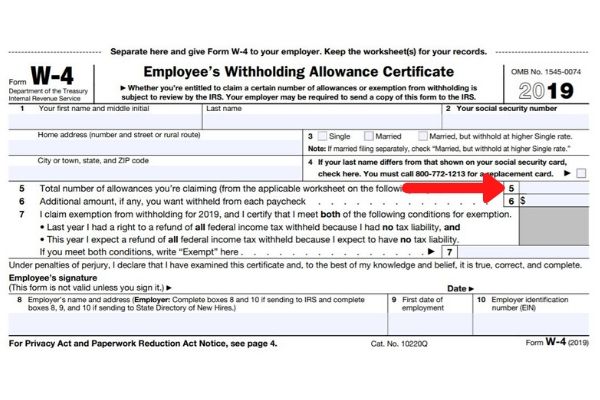

The old W-4 was quite simple and gave employees the option to list a number of “allowances” in Box 5. That number corresponded to a certain dollar amount that would be withheld from the employee’s paycheck for their income tax withholding. The lower the number in box 5, the more taxes that were withheld. The higher the number, the less money that was withheld for taxes.

It was quite common for some people to list “0” in Box 5 (and sometimes even an additional dollar amount in Box 6) to ensure that they would pay the government all their required taxes. They would then get any overpayment back in the form of a tax “refund” the following year.

The new W-4, which was effective Jan 2020 per the Tax Cuts Job Act, is a complete overhaul. The IRS has eliminated Box 5 and the “allowances” all together. Now, there are 5 steps instead of 2 boxes. The reasoning behind this overhaul is to help households calculate their tax withholding more accurately so that people aren’t receiving such large “refunds” and that they can get their money at the time their paychecks are issued versus waiting until the spring of the following year.

There has been a lot of confusion surrounding the new W-4, so let’s break it down, step-by-step.

A breakdown of the New W-4

Step 1:

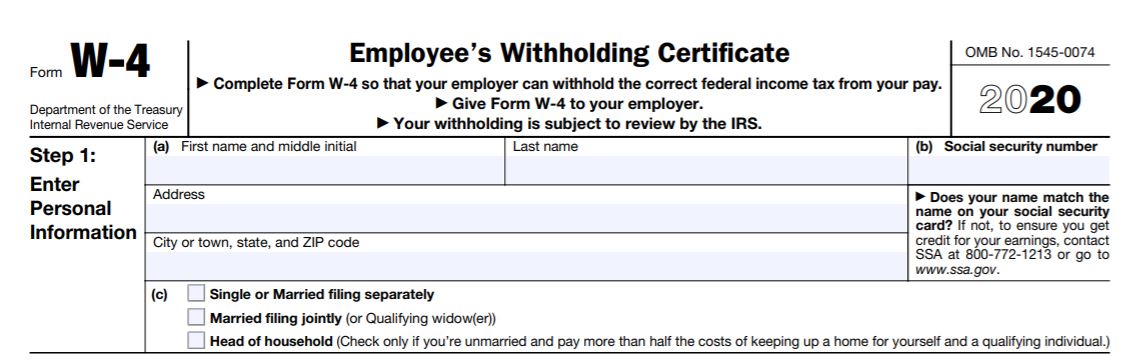

This top section is pretty straightforward. This is where your employee will list all of their personal information: name, address, marital status, and social security number.

Section (c) of Step 1 will determine the amount of tax that should be withheld from an employee’s pay. By checking the appropriate box the payroll provider will know which amount to withhold. All of Step 1 is required information.

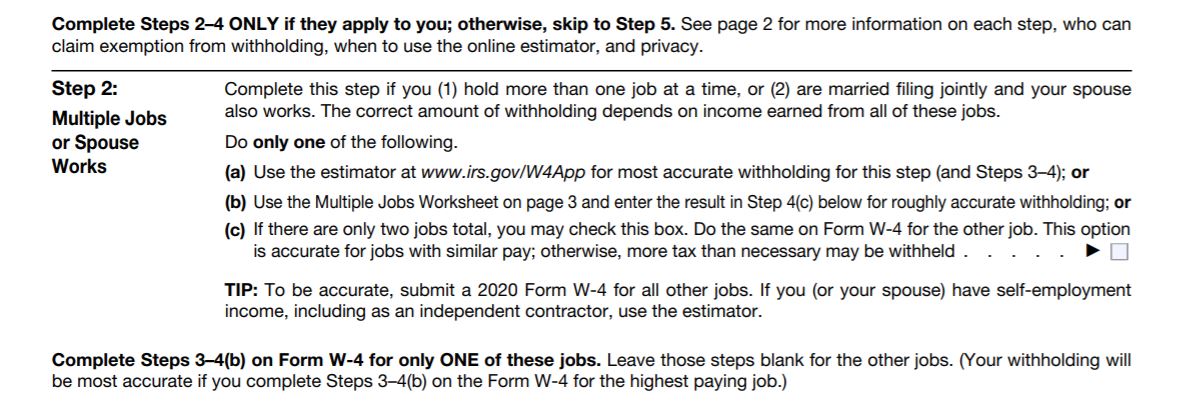

Step 2:

This step is only required if it applies to your employee’s situation. If it does not, it can be skipped and they can move on to step 5 where they sign and date the form. This step (Step 2) would not apply to your employee if their employment with your business was their only job. Step 2 is applicable if your employee has more than one job, or they’re married and filing jointly and their spouse also works.

For Step 2 your employee would use one of the following methods to determine a more accurate federal withholding amount.

Option 2(a) takes your employee to an application that will evaluate their current withholding to determine if you, as their employer, will be withholding enough to meet their tax requirements. This is a good resource if they have existing employment numbers and data to enter into the tool. (Many of which are required data so it’s best to have them on hand prior to filling it out.)

This is NOT a tool for those who are just starting to work for a new employer and are trying to determine their income tax withholding requirements per paycheck. This does not help estimate a person’s income tax that needs to be withheld. It simply analyzes the amount that is currently being withheld based on previous payroll information and lets a person know if it’s sufficient for their tax situation or not.

In order to override the automatic dollar amount that will be withheld from your employee’s paycheck based on what they check in Step 1, an employee would take their information from Step 2(a) and enter it in box 4c.

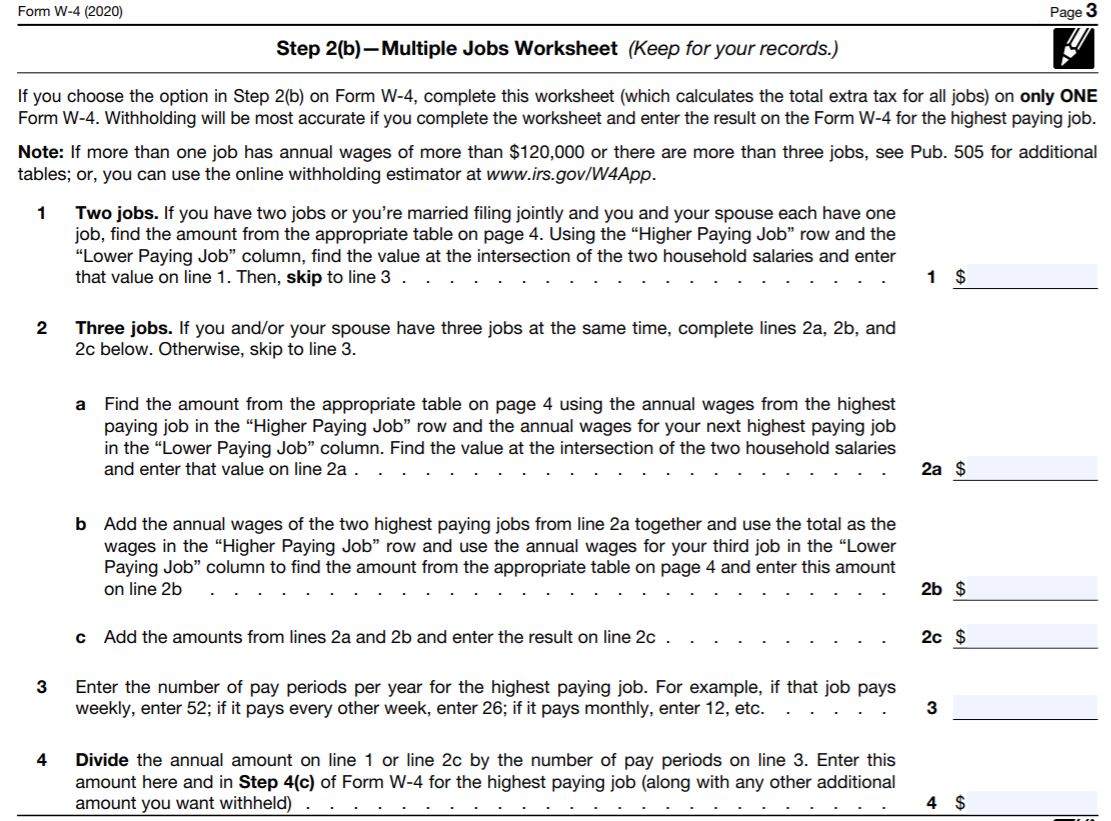

Option 2(b) takes a person to a worksheet on page three:

If your employee is looking for a more accurate number for their federal income tax withholding, this option will get them a number they can place in Box 4c. This worksheet is fairly straightforward and references the Tables on Page 4. The tables can be overwhelming and confusing for someone who hasn’t studied the form or who isn’t familiar with the subject matter. We’ll talk more in depth on the tables below.

Employers, this form is mandatory if you have a payroll. And if you’re an employee and have multiple jobs, or you file with your spouse and you both work – you need a W-4 for each job held. For example, If you’re married and filing jointly and both you and your spouse work, you would use this section 2(b) worksheet for the job that pays the higher amount, but you would still fill out a Form W-4 for the lower paying job as well.

Once you or your employee have a number in box 4 of this worksheet it can be transferred to Box 4(c) on page 1.

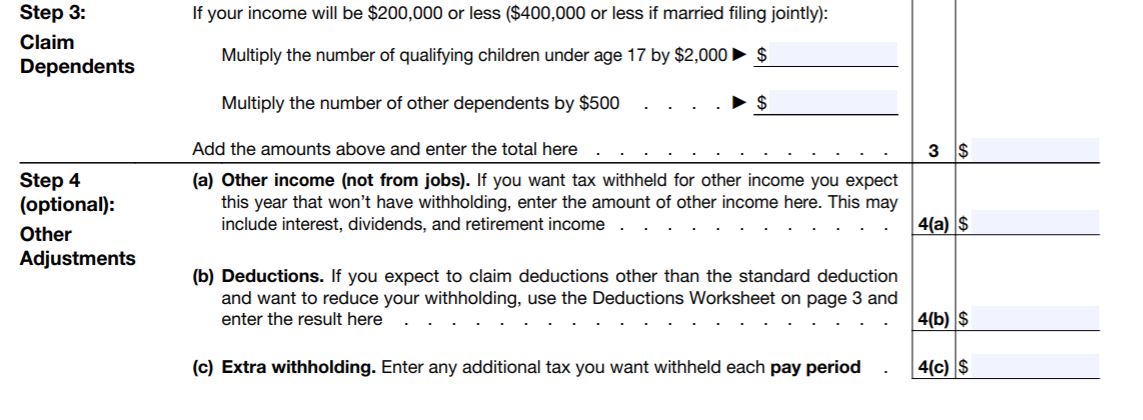

Step 3:

Step 3 is pretty straightforward and instructs people to claim the deductions for their dependents. For example, per the form, if your employee’s income is <$200,000 (or <$400,000 married filing jointly) and they have 2 children they can claim as dependents, they take 2 kids x $2,000 and list $4,000 in box 3 of Step 3.

This dollar amount will LOWER the amount of taxes your employee will have withheld by the dollar amount listed in box 3

Step 4:

We’re back in potentially confusing territory, again.

In Step 4 (a), (b) and (c) your employee will enter other income they want taxed, deductions they want to claim and extra withholding.

Step 4(a) allows an employee to have tax withheld from your payroll for other income they know they will receive from interest, dividends, or retirement income. This will likely not affect a large majority of your employees if you’re a small business owner.

Step 4(b) will apply to only about 3% of the population. The new tax law has been written in such a way that going forward, very few people will itemize their deductions. This box is for individuals who plan to itemize versus take the standard deduction. The employee would list the deduction they would want to claim to reduce their withholding.

Step 4(c) is for extra withholding that is to be withheld from an employee’s paycheck per pay period. This would be similar to box 6 of the old W-4. If you want to claim the max amount to be withheld PLUS have an additional amount withheld, your employee would list that dollar amount here. Remember – it should be written as a dollar amount per paycheck.

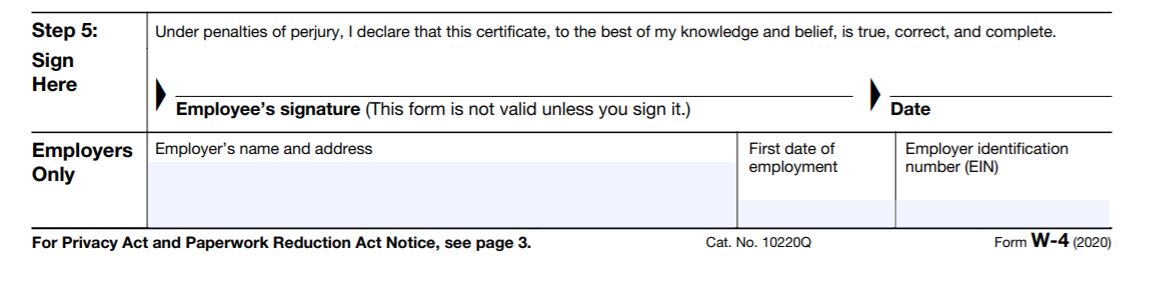

Step 5:

Finally, a really easy step! Here your employee signs and dates the form. The employer should fill in the appropriate employer information.

Almost done.

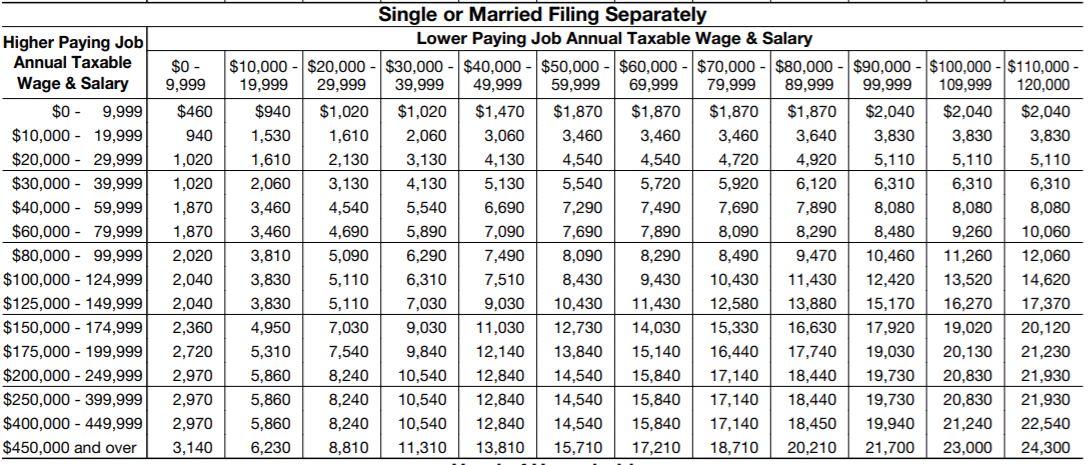

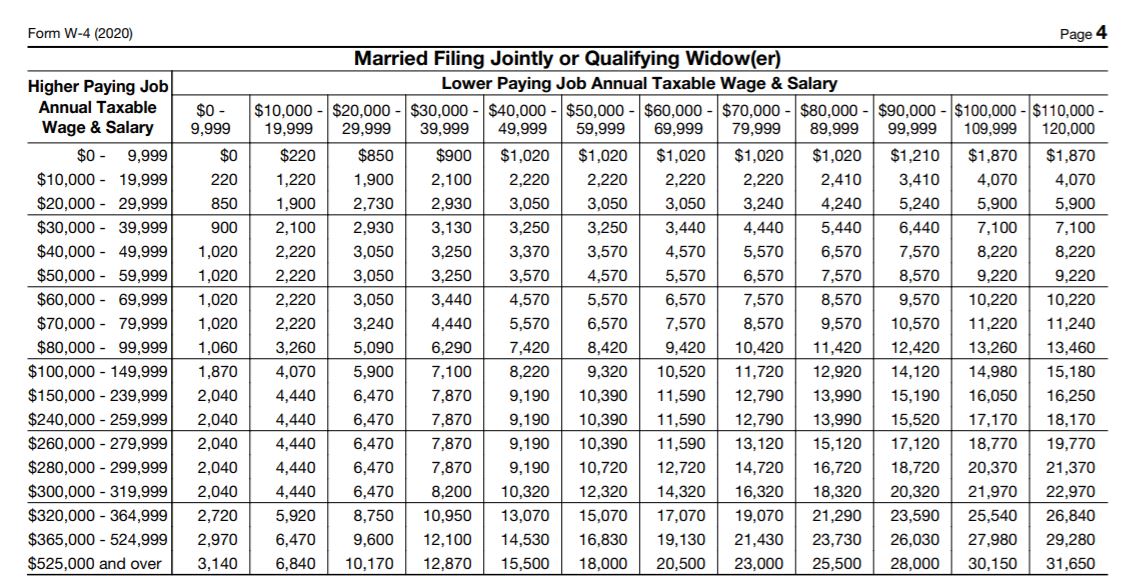

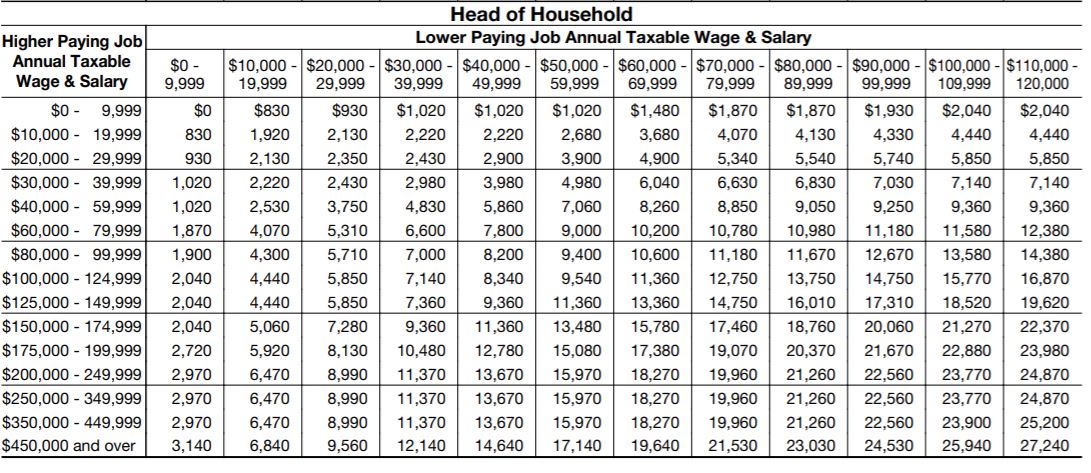

Now let’s talk about how to use those tables on Page 4 of the new W-4 form.

The form advises to use these in Step 2(b) to calculate ‘extra withholding’ for Step 4(c).

The tables themselves are kind of overwhelming since they appear to have the same information across both axises.

But essentially, if your employee has two jobs, they use the left column for the higher paying job and the top row for the lower paying job, and pick the anticipated income for each and where the axis is, is how much extra tax you should withhold in Step 4(c).

These worksheets can also be a simple and easy way for your employee to determine if the amount they are having withheld per paycheck is accurate for their tax responsibilities.

Remember: As an employer you should never tell your employees how to fill out the W-4. You can inform them of what fields you require (1 & 5) but remind them that you’re not a CPA, you’re not allowed to give financial or accounting advice and that they should ask their tax accountant how to fill out the form for the best possible withholding outcome.

We have a feeling that employees will ask how to do the equivalent of claiming 0. In order to do that they simply check their box at the top in Step 1 and Sign and Date in Step 5 and the payroll provider will withhold the max.

If you have questions on how to fill out the new W-4 as an employer or employee please don’t hesitate to call us! We are here to help!

Experience & Expertise

Helping you protect what is most important to you is another way that our firm is here

to serve you and is always on target.